Last reviewed: May 2026

Quick answer: Transactions post out of order because banks record them when they settle through payment networks — not when you make the purchase. Settlement timing depends on merchant batching, authorization delays, processing cutoffs, and overnight posting cycles, which means newer purchases can sometimes post before older ones.

OnlineBankingHelp.com is an independent educational resource. We do not access bank accounts or reverse posted transactions. For account-specific questions, contact your bank directly.

Quick Posting Order Reference

- Most common cause: merchants settle transactions at different times

- Pending transactions: do not determine final posting order

- Restaurants and hotels: often settle later than retail purchases

- Overnight posting: most transactions finalize during batch processing

- Out-of-order posting: usually normal behavior

- High-to-low posting: historically common but less widespread today

- Posting date: matters more than purchase time

Important: A transaction appearing pending does not guarantee it will post next. Final posting order depends on settlement timing and batch processing.

Check These Things First

Before assuming something is wrong with your account, confirm which situation applies:

- A newer purchase posted before an older purchase

- Your balance changed overnight without new activity

- A pending charge disappeared and later reappeared

- A restaurant or hotel charge posted days later

- An overdraft happened on a purchase you made earlier

All of these situations are consistent with normal transaction settlement behavior. The sections below explain exactly why they happen.

Transaction Date vs Posting Date — The Core Difference

The biggest source of confusion is assuming transactions post based on when you make the purchase. Banks do not use purchase time to determine final posting order.

Transaction date: when the purchase or authorization occurs.

Posting date: when the transaction settles and permanently records in your account ledger.

These two events can occur hours or days apart. Until settlement finishes, the transaction remains pending and can move relative to other transactions settling at different times.

This gap between authorization and settlement is the root cause of most out-of-order posting behavior.

Authorization vs Settlement

When you swipe your card or submit a payment online, the bank first receives an authorization request. This verifies that funds or credit are available and creates the pending transaction visible in your account.

The transaction does not fully post until the merchant later submits the finalized settlement request through the payment network.

This means:

- Authorization happens first

- The transaction appears pending

- The merchant later submits settlement data

- The bank posts the finalized transaction

Because settlement timing varies by merchant and payment processor, posting order often differs from purchase order.

This is also why some pending charges disappear temporarily before reappearing as finalized posted transactions.

Why Transactions Settle at Different Times

Settlement timing is controlled primarily by merchants and payment processors — not your bank.

Different businesses finalize transactions at different speeds depending on their systems and workflows.

Transactions That Often Settle Quickly

- Gas stations

- Convenience stores

- Large retail chains

- Automated online payment systems

- Real-time payment networks

Transactions That Often Settle Slowly

- Restaurants waiting to finalize tips

- Hotels holding charges until checkout

- Car rentals holding deposit authorizations

- Subscription services batching charges

- Online merchants waiting for shipment confirmation

This is why a Saturday online purchase may post before a Friday restaurant transaction. The online merchant settled faster even though the restaurant purchase happened earlier.

Authorization Holds vs Final Charges

Some merchants place temporary authorization holds before submitting the final settlement amount.

This is especially common with:

- Gas stations

- Hotels

- Restaurants

- Rideshare services

- Car rental companies

The authorization temporarily reduces your available balance, but the final posted amount may arrive later and in a different amount once settlement completes.

Examples include:

- Restaurant tips added after the meal

- Gas stations preauthorizing larger fuel amounts

- Hotels adding taxes or incidental charges

- Rideshare apps adjusting for route or time changes

This is why pending amounts sometimes differ from the final posted transaction.

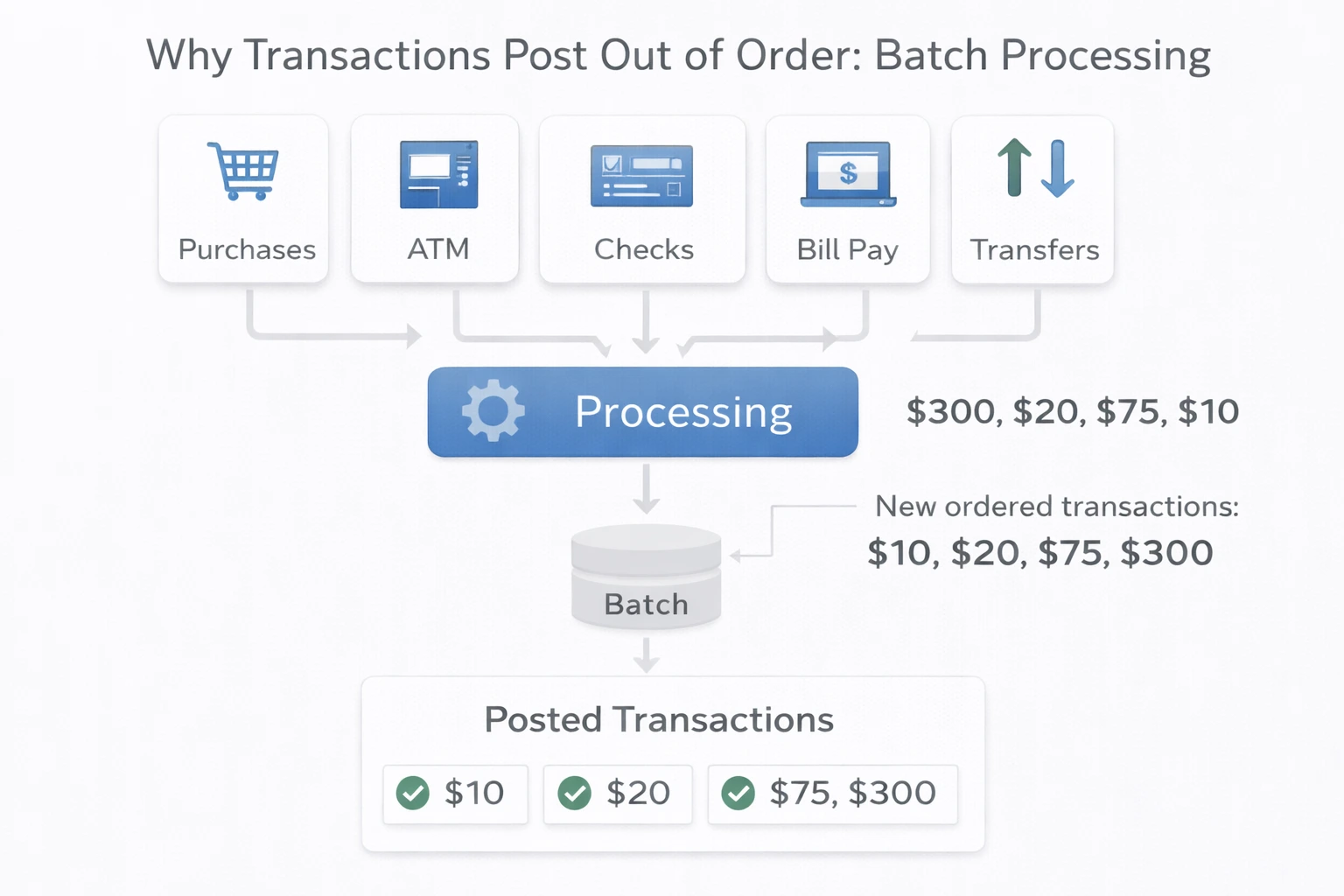

How Batch Processing Determines Posting Order

Banks do not post transactions one by one continuously throughout the day. Most transactions arrive in settlement batches from payment networks and process during scheduled posting cycles.

Most banks run major posting cycles overnight.

During these cycles:

- Settlement files arrive from payment networks

- Pending transactions finalize

- Balances reconcile

- Posted transactions update

- Available balances refresh

Transactions post in the order settlement data arrives within the batch — not necessarily the order you made purchases.

This is one reason balances often change overnight rather than continuously during the day.

See: bank processing times explained.

Example Timeline: Why a Newer Purchase Posts First

| Time | Event |

|---|---|

| Friday 7 PM | Restaurant purchase authorized |

| Saturday 10 AM | Online retailer purchase authorized |

| Saturday 4 PM | Online retailer settles transaction |

| Sunday 2 AM | Online purchase posts |

| Sunday 11 PM | Restaurant settles after tip finalization |

| Monday 3 AM | Restaurant purchase posts |

Even though the restaurant purchase happened first, the online purchase posted first because its settlement data reached the bank earlier.

How Banks Apply Internal Posting Rules

Beyond merchant settlement timing, banks also apply their own internal posting-order rules during processing cycles.

Common posting rules include:

- Deposits and credits posted before debits

- Transactions grouped by payment type

- Chronological posting within settlement groups

- Real-time posting for certain transaction types

- Separate handling for ACH, card, and check transactions

These rules vary by institution and are usually disclosed in the account agreement.

Most major banks today post transactions based largely on settlement arrival order rather than highest-to-lowest dollar amount posting.

The History of High-to-Low Posting

Many customers became suspicious of out-of-order posting because major banks historically used a practice called high-to-low posting.

Under this system, banks deliberately posted the largest transactions first within each processing batch to maximize overdraft fees.

Example:

- Account balance: $100

- Four small $20 purchases

- One $120 purchase

If the $120 transaction posted first, all smaller purchases could also overdraft afterward — generating multiple overdraft fees instead of one.

This practice triggered class action lawsuits against major banks including Bank of America, Wells Fargo, TD Bank, and US Bank during the 2010s. Regulatory pressure from the Consumer Financial Protection Bureau (CFPB) and other agencies pushed many banks to revise their posting policies.

Today, most out-of-order posting is caused by settlement timing and batch processing rather than intentional fee maximization.

Why Out-of-Order Posting Causes Overdrafts

Out-of-order posting becomes most problematic when account balances are low.

Example:

- Monday morning: $15 coffee purchase

- Monday afternoon: $200 grocery purchase

- Tuesday: coffee settles and posts

- Wednesday: other transactions reduce balance

- Thursday: grocery transaction finally settles and posts

Even though the grocery purchase happened earlier, it posted later when the account balance was lower. From the bank’s perspective, the overdraft reflects the posting balance — not the purchase-time balance.

This is one of the most common causes of “I had the money when I bought it” overdraft complaints.

Debit Cards vs Credit Cards — Do They Post Differently?

Debit and credit card transactions follow similar authorization and settlement structures, but they affect balances differently.

Debit card transactions: reduce your available balance almost immediately because they pull directly from your bank account.

Credit card transactions: usually affect available credit rather than your checking account balance, even though settlement timing still works similarly behind the scenes.

Because debit transactions directly affect available funds, out-of-order posting creates more noticeable balance and overdraft issues on debit accounts than on credit cards.

Why Pending Transactions Sometimes Disappear

Pending transactions can temporarily disappear for several reasons:

- The authorization expired before settlement arrived

- The merchant reversed and reissued the transaction

- The payment network refreshed the authorization

- The merchant submitted final settlement later

- The transaction was canceled entirely

In many cases, the pending authorization disappears briefly and then reappears as a finalized posted transaction later.

See: why pending transactions disappear.

What You Can Do About Out-of-Order Posting

Track Spending Independently

Your available balance reflects pending authorizations, but it cannot predict the exact order future settlements will post. Tracking purchases independently reduces overdraft surprises.

Maintain a Balance Buffer

Keeping extra funds above your minimum needed balance is the safest protection against overdrafts caused by delayed settlement timing.

Enable Transaction Alerts

Most banking apps offer push notifications when pending transactions post. This makes it easier to monitor overnight posting cycles.

Understand Your Bank’s Posting Rules

Your account agreement explains how your bank applies settlement batches and posting order policies.

When Out-of-Order Posting Is Normal vs When To Investigate

Usually Normal

- Transactions posting in a different order than purchases

- Restaurants posting days later

- Balances changing overnight

- Pending authorizations disappearing temporarily

- Final amounts adjusting slightly from pending amounts

Potential Problems

- Duplicate posted charges

- Posted transactions disappearing permanently

- Large unexplained amount differences

- Unknown merchants appearing

- Balance reductions without visible transactions

If something appears genuinely incorrect, contact the bank and dispute the transaction directly.

Frequently Asked Questions

Why do my transactions post out of order?

Transactions post out of order because banks record them when they settle rather than when you make the purchase. Settlement timing depends on merchants, payment processors, and overnight batch systems, which means newer transactions can sometimes settle before older ones.

What is the difference between transaction date and posting date?

The transaction date is when the purchase or authorization occurs. The posting date is when the bank finalizes and permanently records the transaction after settlement completes. These dates may differ by hours or days.

Do banks intentionally reorder transactions?

Most major banks today generally post transactions based on settlement timing rather than intentionally reordering them. However, high-to-low posting practices were historically common and resulted in lawsuits and regulatory pressure during the 2010s.

Why did an overdraft happen on a transaction I made earlier?

The overdraft reflects when the transaction posted rather than when the purchase occurred. If the account balance declined before the delayed transaction finally settled, the later posting could trigger an overdraft even though you originally had sufficient funds.

Why do restaurant and hotel charges post later?

Restaurants often wait to finalize tips before settlement, while hotels hold authorizations until checkout and final billing. These industries commonly delay settlement compared to standard retail purchases.

Why does my balance change overnight?

Most banks run overnight batch-processing cycles where pending transactions finalize, settlement files import, balances reconcile, and posted transactions update. This causes many balance changes to appear overnight instead of instantly.

Can pending transactions disappear and come back?

Yes. Pending authorizations sometimes expire, refresh, or temporarily disappear before the merchant submits final settlement. The finalized posted transaction may later reappear in a different position within the transaction history.

Can I control the order my transactions post?

No. Posting order depends on settlement timing, payment-network processing, merchant batching, and the bank’s internal posting systems. Customers cannot manually control transaction posting order.

Related Banking Guides

- Why bank transactions stay pending

- Why pending transactions disappear

- Available balance vs current balance

- Bank processing times explained

- Why banks post transactions overnight

- Bank holds explained

Bottom Line

Transactions post out of order because banks finalize transactions when settlement data arrives — not when purchases happen. Merchant batching, authorization holds, overnight processing cycles, and payment-network timing all influence when transactions actually post.

What appears to be “random” posting behavior is usually the result of normal settlement systems operating behind the scenes. Restaurants, hotels, online merchants, subscription services, and gas stations all process settlement differently, which changes final posting order.

The safest approach is monitoring your available balance, maintaining a balance buffer, and understanding that pending transactions do not guarantee final posting sequence. If transactions appear genuinely incorrect rather than simply out of order, contact your bank and dispute the activity directly.