Seeing a debit card purchase change amount after it was already pending can feel unsettling. A charge you recognized suddenly increases, decreases, or finalizes at a different number than expected.

This behavior is one of the most misunderstood parts of banking. It is not a bank error, a delay, or a processing glitch. In most cases, it is a normal part of how merchants estimate charges and submit final totals.

OnlineBankingHelp.com is an independent educational resource and does not access accounts or provide account-specific support.

Why this happens so often

Debit card amount changes are most common in situations where the final total is not known at the time of purchase.

- Gas stations

- Restaurants and bars (tips)

- Hotels

- Car rentals

- Ride shares and delivery services

In these cases, the merchant sends an estimated authorization first, then submits the final amount later.

What an estimated authorization really is

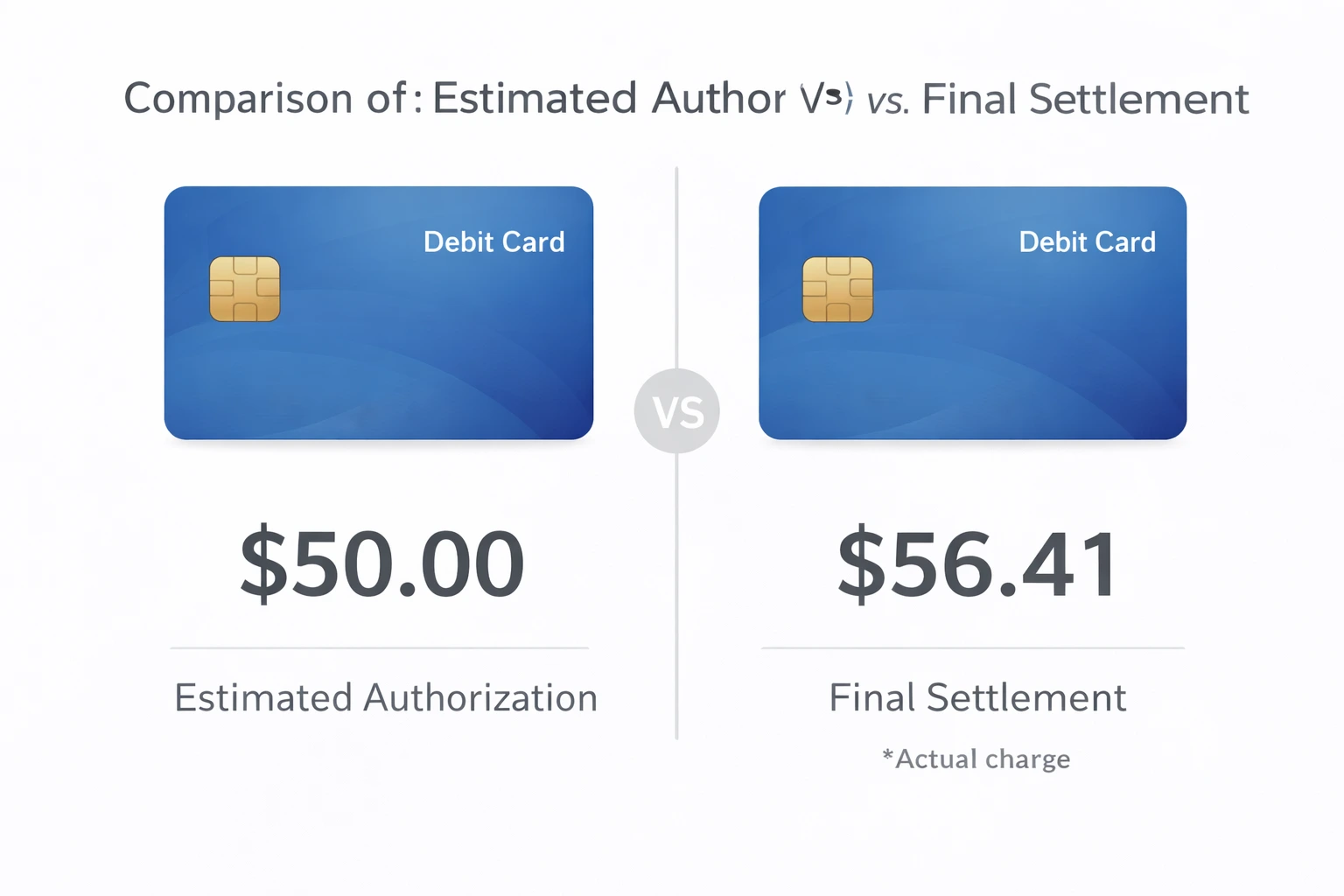

An estimated authorization is a temporary amount the merchant requests to confirm your card is valid and has sufficient funds.

This is not the final charge. It is a placeholder designed to protect the merchant while the transaction is completed.

Common examples include:

- Gas stations authorizing $75–$200 before fueling

- Restaurants authorizing the bill before tip is added

- Hotels authorizing room rate plus incidentals

The estimated amount appears as pending and temporarily reduces your available balance.

Why the final amount changes after pending

Once the merchant knows the true total, they submit the final settlement amount.

That final amount can be:

- Higher than the pending amount (tip added, full fuel amount)

- Lower than the pending amount (unused authorization released)

- Exactly the same

When settlement occurs, the pending authorization is removed and replaced with the finalized charge. This is when people notice the amount “change.”

Pending does not mean final

A pending transaction is not locked in.

Pending status only means the merchant has requested authorization. It does not represent the final amount and does not guarantee what will ultimately post.

This distinction is critical to understanding debit card behavior and is closely related to how banks separate balances. See available balance vs current balance explained for a deeper breakdown.

This is merchant behavior, not bank timing

Amount changes after pending are driven by the merchant, not the bank.

The bank does not adjust the amount on its own. It posts exactly what the merchant submits at settlement. If the amount changes, it is because the merchant finalized a different total than the estimate.

This behavior is distinct from delays caused by processing schedules or posting windows, which are explained in bank processing times.

Why this can cause confusion or overdrafts

Estimated authorizations reduce your available balance immediately, but the final amount may post later.

If the final amount is higher and posts when fewer funds are available, it can trigger an overdraft even though the original pending amount seemed safe.

This timing mismatch is similar to other posting behaviors explained in why banks post transactions overnight and why transactions post out of order.

What this is not

It is important to separate debit card amount changes from other banking concepts.

- This is not a bank hold (bank holds explained)

- This is not a pending transfer issue (why bank transfers get delayed)

- This is not ACH processing or settlement timing

This is a normal part of how card-based merchant transactions work.

How to reduce surprises from debit card authorizations

- Leave extra buffer when paying at gas stations or hotels

- Remember tips are added after authorization

- Monitor available balance, not just posted balance

- Use credit cards for high-authorization merchants when possible

Understanding that pending amounts are estimates—not promises—helps prevent confusion and unnecessary stress.

The system intent behind changing amounts

Debit card systems are designed to balance merchant protection with customer access.

Estimated authorizations allow transactions to happen smoothly when totals are unknown. Final settlement corrects the estimate once certainty exists. The amount change is not a mistake—it is the system completing the transaction accurately.

Once you understand that pending charges are estimates and final posting reflects reality, these changes stop feeling random. They are simply the system finishing the job.