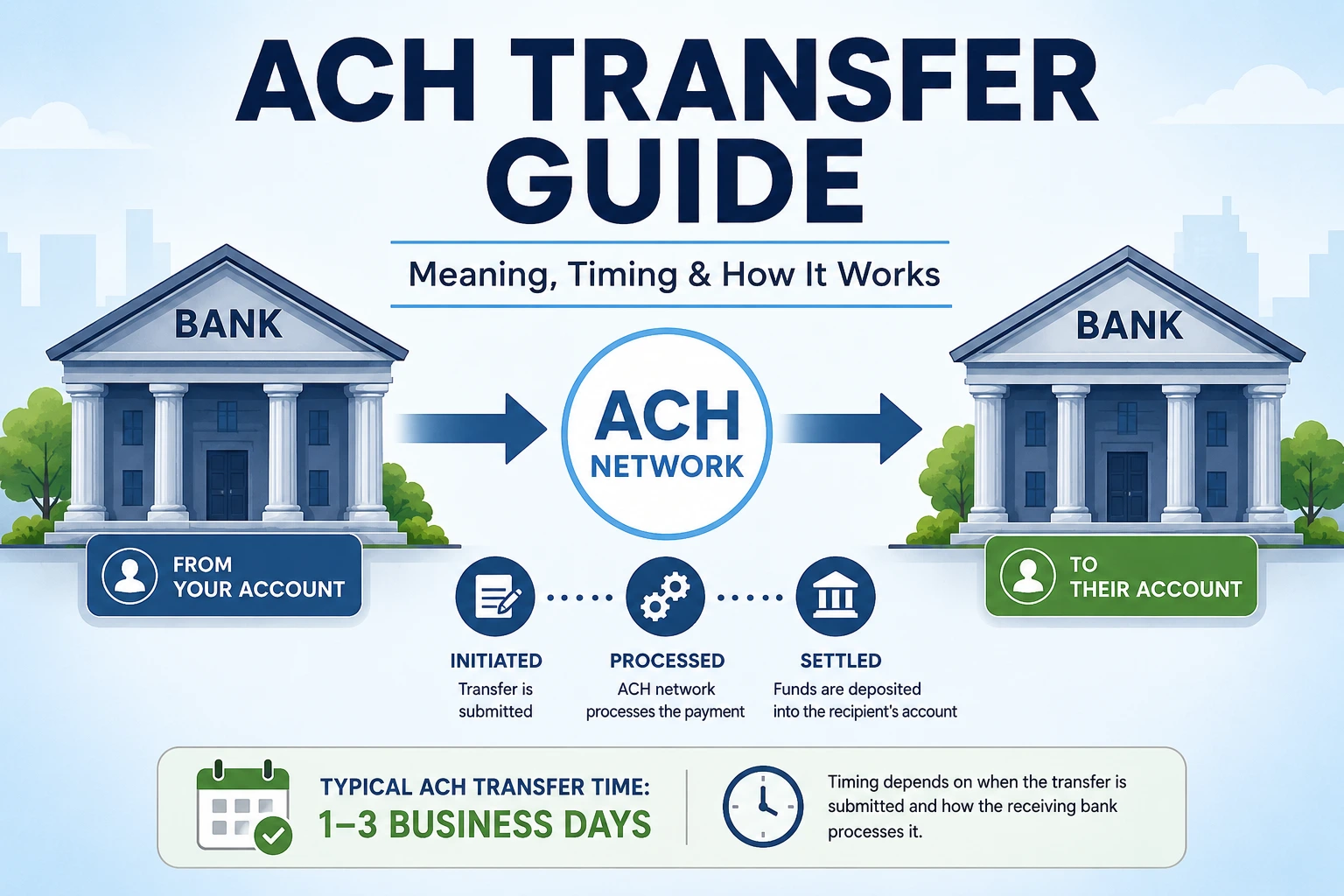

Quick answer: An ACH transfer is an electronic bank-to-bank payment processed through the Automated Clearing House network. Most ACH transfers take 1 to 3 business days and are processed in scheduled batches rather than in real time.

ACH transfers power many everyday banking activities, including direct deposits, bill payments, and transfers between accounts. While they are reliable and widely used, they are not always instant.

If you are waiting on a transfer, you may also want to review why transactions stay pending and how long bank transfers take.

What Is an ACH Transfer?

ACH stands for Automated Clearing House, a nationwide network used by banks and credit unions to send and receive electronic payments.

Unlike wire transfers, ACH payments are grouped together and processed at scheduled times, which helps reduce costs but adds processing delays.

This system design is explained in why ACH transfers are processed in batches.

Common Examples of ACH Transfers

- Direct deposit from employers or government payments

- Paying bills through online banking

- Transfers between your own bank accounts

- Recurring subscriptions and automatic payments

- Transfers initiated by apps like PayPal or Venmo

Types of ACH Transfers

There are two types of ACH transfers, and understanding the difference helps explain how and when money moves.

- ACH credit: Money is pushed from your account to another account. You initiate the transfer. Common examples include sending money to another person or moving funds between your own accounts at different banks.

- ACH debit: A company or individual pulls money from your account. You authorize this in advance. Common examples include utility bill autopay, gym memberships, and loan repayments.

Both types follow the same batch processing system, which explains why transfers often take time to complete.

How Long Does an ACH Transfer Take?

Most ACH transfers complete within 1 to 3 business days, depending on when the transfer is submitted and how the receiving bank processes it. Same-day ACH is available at many banks for transfers submitted before the cutoff time.

- ACH credits: Typically 1 to 2 business days

- ACH debits: Often next business day

- Same-day ACH: Available for eligible transfers submitted before cutoff

For a full breakdown of timing across all transfer types, see how long bank transfers take.

Even after funds appear, final posting may occur during overnight cycles. Learn more in why banks post transactions overnight.

ACH Transfer Timing Examples

| Transfer Submitted | Typical Arrival | Why |

|---|---|---|

| Monday morning | Tuesday | Processed in same-day or next-day batch |

| Monday evening (after cutoff) | Wednesday | Misses Monday batch, enters Tuesday’s |

| Friday afternoon | Monday or Tuesday | Weekend pause; resumes Monday |

| Saturday | Monday or Tuesday | Most banks do not process Saturday ACH |

| Day before a federal holiday | One additional business day | ACH network pauses on federal holidays |

ACH Processing Schedule

The ACH network operates on a defined schedule set by Nacha, the governing body for ACH payments. Understanding these windows helps explain why transfers submitted at certain times take longer than expected.

| Transfer Type | Submission Cutoff | Funds Available | Notes |

|---|---|---|---|

| Same-day ACH | Typically 10:30 AM, 2:45 PM, or 4:45 PM ET (varies by bank) | Same business day | Additional fee may apply; not all banks participate |

| Next-day ACH credit | Typically by 5:00–8:00 PM ET | Next business day | Most common for direct deposit |

| Standard ACH credit | Varies by bank | 1–2 business days | Default for most bank-to-bank transfers |

| ACH debit | Varies by originator | Next business day | Used for bill pay, subscriptions |

Cutoff times vary by financial institution. If your bank’s cutoff is 5:00 PM ET and you submit at 5:30 PM, the transfer enters the next available batch. See what time bank transfers process for a deeper look at cutoffs.

Same-Day ACH

Same-day ACH was introduced by Nacha in 2016 and has been expanded several times since. It allows eligible transfers to be processed and settled within the same business day rather than the standard 1 to 3 day window.

How same-day ACH works

- The transfer must be submitted before your bank’s same-day cutoff, typically between 10:30 AM and 4:45 PM ET depending on the processing window

- Both the sending and receiving banks must participate in same-day ACH

- The current per-transaction limit for same-day ACH is $1,000,000 (raised by Nacha in 2022)

- A small fee is typically charged by the originating bank, though many consumer banks absorb this cost

What same-day ACH is commonly used for

- Payroll for hourly or on-demand workers

- Urgent bill payments to avoid late fees

- Business-to-business disbursements

- Insurance claim payments

Not all consumer transfers qualify for same-day processing. International ACH transactions (IATs) are excluded. If your bank does not offer same-day ACH, the transfer will default to standard timing.

Weekend ACH Processing

While ACH processing capabilities have expanded in recent years, most consumers still experience ACH transfers as a business-day service. Transfers submitted on weekends may not fully settle until the next business day, and weekend processing or funds availability varies by bank, credit union, and payment provider.

What happens to ACH transfers on weekends

- If your bank participates in weekend ACH: Transfers submitted Friday evening or Saturday morning may settle Saturday or Sunday

- If your bank does not participate: Transfers submitted after Friday’s cutoff will not begin processing until Monday morning

- Direct deposit: Some employers and payroll processors now support Saturday direct deposit, but Sunday settlement is less common

In practice, most consumers still experience weekend delays. A transfer submitted Friday afternoon will typically post Monday or Tuesday. For more detail, see why transfers stay pending over the weekend.

Holiday ACH Processing

The ACH network does not process transfers on federal banking holidays. When a holiday falls on a weekday, it effectively adds one business day to standard transfer timelines.

Federal holidays that pause ACH processing

- New Year’s Day

- Martin Luther King Jr. Day

- Presidents’ Day

- Memorial Day

- Juneteenth

- Independence Day

- Labor Day

- Columbus Day

- Veterans Day

- Thanksgiving Day

- Christmas Day

Holiday timing examples

- Transfer submitted the day before a holiday: Processing pauses on the holiday and resumes the next business day, adding one day to the expected timeline

- Payroll landing on a holiday: Employers should originate payroll two business days early to ensure funds arrive on time; many do not, causing delays

- Holiday weekend: A Monday holiday combined with a weekend can delay a Friday transfer by up to four days

For more on how bank schedules affect transfer timing, see bank processing times explained.

ACH vs Instant Payment Networks

Many consumers compare ACH transfers to services such as Zelle, FedNow, and RTP (Real-Time Payments). While ACH remains the most widely used bank-to-bank transfer system in the United States, it was designed for high-volume batch processing rather than instant settlement.

| Network | Typical Speed | Availability |

|---|---|---|

| ACH | 1–3 business days | Most banks and credit unions |

| Same-Day ACH | Same business day | Participating institutions |

| Zelle | Minutes | Participating banks |

| FedNow | Seconds | Growing bank participation |

| RTP | Seconds | Participating financial institutions |

Although instant payment networks are growing rapidly, ACH continues to handle billions of transactions annually because of its reliability, low cost, and widespread adoption.

Bank-by-Bank ACH Timing Examples

While all banks use the same ACH network, their individual processing schedules, cutoff times, and funds availability policies vary. The table below reflects general patterns based on publicly available information. Always confirm current details with your bank directly.

| Bank | Standard ACH Timeline | Same-Day ACH Available | Outgoing Cutoff (approx.) |

|---|---|---|---|

| Chase | 1–2 business days | Yes | 8:00 PM ET |

| Bank of America | 1–3 business days | Yes | 5:00 PM ET |

| Wells Fargo | 1–3 business days | Yes | 5:00 PM PT |

| Citibank | 1–3 business days | Yes (select accounts) | 5:30 PM ET |

| US Bank | 1–3 business days | Yes | 6:00 PM CT |

| Ally Bank | 1–3 business days | No (standard only) | 7:30 PM ET |

| Marcus by Goldman Sachs | 1–3 business days | No | Varies |

| Credit unions (general) | 1–3 business days | Varies by institution | Varies |

Cutoff times and same-day eligibility change periodically. If speed matters, confirm current processing windows with your bank before initiating a transfer.

What Affects ACH Transfer Timing?

- Submission time and cutoff windows

- Weekends and federal holidays

- Bank processing schedules

- Fraud and security checks

- Account history and risk factors

Because ACH processing pauses on non-business days, transfers may remain pending longer than expected. See why transfers stay pending over the weekend.

For a deeper look at what causes delays specifically, see why bank transfers get delayed.

Why ACH Transfers Show as Pending

A pending ACH transfer means the payment has been accepted but not fully processed or posted yet.

- Batch processing has not completed

- The transfer was submitted after cutoff time

- The receiving bank has not finalized posting

- Security checks are in progress

This stage is explained in more detail in why transactions stay pending.

If delays continue, they may be related to bank holds and funds availability or transfer delays and processing issues.

ACH Transfer Limits

Banks and credit unions often place limits on ACH transfers to reduce fraud risk and manage account security. These limits vary by institution and may depend on your account type, account history, and whether the transfer is incoming or outgoing.

Consumer banks commonly set ACH transfer limits ranging from a few thousand dollars per day to tens of thousands of dollars per day. Business accounts typically have higher limits.

- Daily transfer limits: Maximum amount that can be transferred in a single day

- Monthly transfer caps: Limits on total ACH activity during a month

- New account restrictions: Lower limits may apply until an account establishes a history

- Incoming vs. outgoing limits: Banks often allow larger incoming transfers than outgoing transfers

- External transfer limits: Transfers to accounts at other banks may have stricter limits than internal transfers

If you need to move a large amount of money, your bank may allow a temporary limit increase. For very large or time-sensitive transactions, a wire transfer may be a better option.

ACH vs Wire Transfers

ACH and wire transfers both move money electronically, but they work very differently. The right choice depends on how fast you need the funds to arrive and how much you are willing to pay.

| ACH Transfer | Wire Transfer | |

|---|---|---|

| Speed | 1–3 business days (same-day available) | Same day, often within hours |

| Cost | Usually free or low cost | $15–$50 outgoing; $0–$15 incoming |

| Processing | Batch; scheduled windows | Real-time; processed individually |

| Reversibility | Can be reversed within 5 banking days in some cases | Generally not reversible once sent |

| Transaction limits | Up to $1,000,000 (same-day ACH); varies by bank for standard | Higher limits; varies by bank |

| International | Domestic only (standard ACH) | Available internationally (SWIFT) |

| Best for | Routine transfers, payroll, bill pay | Large or urgent payments |

ACH transfers prioritize cost efficiency, while wire transfers prioritize speed. For most everyday transfers, ACH is the better option. For large, time-sensitive payments, a wire may be worth the fee.

For a full comparison, see ACH vs wire transfers explained.

When ACH Transfers Make the Most Sense

- Direct deposit of income — see how direct deposit works

- Recurring payments where timing is predictable

- Routine transfers between your own accounts

- Non-urgent payments where cost matters more than speed

Frequently Asked Questions

How long does an ACH transfer take?

Most ACH transfers take 1 to 3 business days. ACH credits typically arrive in 1 to 2 business days. ACH debits are often processed the next business day. Same-day ACH is available at many banks for transfers submitted before the cutoff time, usually by mid-afternoon ET.

What does ACH transfer mean?

ACH stands for Automated Clearing House. An ACH transfer is an electronic payment sent between bank accounts through the ACH network, which is operated under rules set by Nacha. It is one of the most common ways money moves between banks in the United States, used for direct deposit, bill pay, and account-to-account transfers.

Can ACH transfers be reversed?

In some situations, yes. ACH transfers may be reversed for duplicate payments, incorrect amounts, fraud, or authorization errors. Under Nacha rules, reversals must be initiated within 5 banking days of the original settlement date. After that window closes, recovery typically requires the cooperation of the receiving bank or legal action.

Why is my ACH transfer still pending after 3 days?

Transfers can remain pending due to weekends, federal holidays, cutoff times, security reviews, incorrect account information, or delays at the receiving bank. Most ACH transfers complete within 1 to 3 business days, but some may take longer depending on the institutions involved.

Can ACH transfers arrive on weekends?

Some banks participate in weekend ACH processing introduced by Nacha in 2021, but many consumer transfers still do not fully settle until the next business day. Weekend processing remains less common than weekday processing.

What happens if I enter the wrong account number?

If incorrect account information is entered, the transfer may be rejected and returned or, in rare cases, sent to the wrong account. Contact your bank immediately if you believe an error was made. The sooner you report it, the more options your bank has to recover the funds.

Are ACH transfers safe?

Yes. ACH transfers use banking industry security standards and are widely used for payroll, direct deposits, bill payments, and account-to-account transfers. Banks also monitor ACH activity for fraud and suspicious transactions. Never share your bank account or routing number with unverified parties.

How do I initiate an ACH transfer?

Most banks allow you to initiate an ACH transfer through online banking or a mobile app by adding the recipient’s routing number and account number. Some banks call this a bank transfer, external transfer, or account-to-account transfer. Processing times and cutoff windows vary by institution.

Related Banking Guides

- Why transactions stay pending

- How long bank transfers take

- Bank processing times explained

- Bank holds explained

- Why ACH transfers are processed in batches

- What time bank transfers process

- Why transactions post out of order

- How banks detect suspicious deposits

- Direct deposit guide

- Why bank transfers get delayed

- ACH vs wire transfers explained

Bottom Line

An ACH transfer is one of the most reliable and widely used ways to move money between bank accounts. While it is not instant, it is designed for secure, high-volume processing at low cost.

Understanding the ACH processing schedule, same-day options, and how weekends and holidays affect timing makes it much easier to interpret delays, plan payments, and choose the right transfer method for your situation. If you are setting up regular payments, see how direct deposit works or what causes bank transfer delays for more detail.